Table of Contents

If you’re just starting in tax lien investing, you’ve probably stumbled across the terms “tax deeds” and “tax lien certificates” and wondered what the difference is between tax lien certificates vs tax deeds.

Confusing, right?

But don’t worry—you’re not alone.

I’ve been in your shoes, trying to figure out whether to invest in tax lien certificates or go all in on a tax deed.

Let’s clear things up so you can decide based on what fits your goals.

What’s a Tax Lien Certificate Anyway?

Imagine this: a homeowner hasn’t paid their property taxes, and now the local government is owed some cash.

The government doesn’t want to wait around for the payment, so they sell that “debt” to an investor (you, potentially) in the form of a tax lien certificate.

As the investor, you’re now holding a legal claim to that debt.

Your main goal?

Get paid back by the homeowner, with interest.

If they do, great—you collect your investment plus a nice return.

If they don’t, there’s a chance you could foreclose and own the property.

But that’s pretty rare.

Image Credit: https://www.investopedia.com/terms/t/taxliencertificate.asp

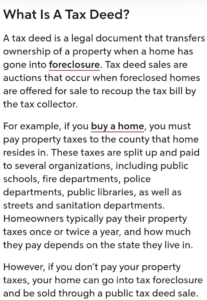

And a Tax Deed?

Now, tax deeds are a bit different.

When the government sells a tax deed, they’re essentially handing over the whole property to the highest bidder.

You’re not just buying the right to collect the debt—you’re buying the actual property.

This is usually done through an auction, and once you win, that property is yours.

Image Credit: https://www.rocketmortgage.com/learn/tax-deed

How Do They Compare?

Let’s break down the key differences so you can see which one makes the most sense for you.

1. Ownership vs. Lien Rights

- Tax Lien Certificates: You’re buying the right to collect unpaid property taxes, not the property itself.

Your main goal is to earn interest from those taxes.

- Tax Deeds: You’re buying the property outright.

If you win the auction, you own the home, land, or commercial space in question.

Tip: If you’re aiming for a steady, interest-based return, tax lien certificates are your go-to.

If you want the potential to own real estate, look into tax deeds.

2. Return on Investment (ROI)

- Tax Lien Certificates: The return comes from the interest or penalties paid by the homeowner.

Depending on state law, this can range from 6% to 24%—not bad compared to other investments.

- Tax Deeds: Here, you make money by reselling, renting, or holding the property.

You might sell it for a profit, fix it up and rent it out, or hold onto it for future appreciation.

Tip: Ask yourself, “Do I want a passive income from interest or active income from real estate activities?”

Your answer will help guide your choice.

3. Redemption Period

- Tax Lien Certificates: There’s a redemption period, typically 1 to 3 years, where the property owner can pay back taxes, interest, and fees to redeem their property.

During this time, you’ll either collect the interest or, if they don’t pay, potentially foreclose.

- Tax Deeds: Usually, there’s no redemption period.

Once you’ve won the auction, the property is yours to do with as you please.

Tip: Tax lien certificates are great if you’re patient and willing to wait out the redemption period.

Tax deeds are for those who want more immediate ownership and control.

4. Risk and Property Ownership Potential

- Tax Lien Certificates: Lower risk because your primary goal is to collect interest.

Foreclosure is possible but uncommon.

- Tax Deeds: Higher risk since you’re taking on full ownership, including any baggage that comes with the property (outstanding liens, repairs, or legal issues).

Actionable Step: Before investing in tax deeds, be ready to take on property management and handle all the responsibilities that come with it.

5. State-Specific Rules

Not all states handle tax liens and tax deeds the same way.

Some states, like California, only sell tax deeds, meaning you’re buying full ownership of the property.

Other states, like Florida, sell tax lien certificates, where you’re primarily earning interest on the unpaid taxes.

Actionable Step: Research your state’s rules.

Make sure you understand the local process for auctions, redemption periods, and interest rates.

6. Investment Time Frame

- Tax Lien Certificates: These are usually a longer-term investment, as you might need to wait through the redemption period before collecting your interest or foreclosing.

- Tax Deeds: You gain ownership right away, but the process doesn’t end there.

You may need to rehab, resell, or find tenants.

Tip: If you’re okay with a slow-burn investment, go with tax lien certificates.

If you’re looking for something a bit more fast-paced, tax deeds might be your thing.

7. Upfront Costs and Capital

- Tax Lien Certificates: Typically lower entry cost.

You’re buying the unpaid taxes, which might be just a few thousand bucks.

- Tax Deeds: Higher upfront cost.

You’ll need to pay the winning bid price to own the property, which can be significantly more.

Actionable Step: Check your budget.

If you’re looking to start small, tax lien certificates might be a better option.

If you’re ready to spend a bigger chunk of change, consider tax deeds.

8. Due Diligence Requirements

- Tax Lien Certificates: Make sure the property has value.

Look into its location, condition, and any other liens.

You don’t want to end up with a useless plot of land or property tied up in legal issues.

- Tax Deeds: Due diligence is even more crucial here since you take full ownership.

Inspect the property, research the title, and check for any outstanding issues that could affect its value.

Actionable Step: Never invest blindly.

Attend local auctions, do your research, and always inspect the property (even if it’s just a drive-by).

Pros and Cons of Tax Lien Certificates and Tax Deeds

Tax Lien Certificates

- Pros:

Lower cost of entry.

Consistent interest returns.

Less hands-on work compared to property ownership.

- Cons:

Illiquid asset—you can’t easily sell the certificate.

Due diligence is still needed to ensure the property has value.

Potentially long waiting period for returns.

Tax Deeds

- Pros:

Opportunity for high profits through resale or rental.

Immediate property ownership.

Potential to acquire property for less than market value.

- Cons:

Higher upfront costs.

Greater risk (property condition, outstanding liens).

Hands-on work required for property management or sale.

Tip: Write out your investment goals.

Are you looking for steady interest income with minimal work (tax lien certificates)?

Or are you ready to roll up your sleeves and dive into real estate (tax deeds)?

What’s Right for You?

It all depends on your investment style, risk tolerance, and financial goals.

Here’s a quick checklist to help you decide:

- Goal-Oriented Approach: Are you looking for steady returns over time? Tax lien certificates might be your thing. Want to take ownership and build real estate wealth? Tax deeds are for you.

- Risk Appetite: Are you willing to take on property issues or the potential for foreclosure? Tax deeds are riskier but more rewarding. Prefer low-risk and stable returns? Stick to tax lien certificates.

- Budget and Timeframe: Smaller budget and willing to wait it out? Go for tax liens. Larger budget and want faster control? Tax deeds are your play.

Practical Tips for Getting Started

- Know Your State Laws: Research how tax lien and tax deed sales are handled in your state. Understanding your local market is half the battle.

- Attend Auctions: Whether in person or online, sit in on a few auctions before bidding. It’s a great way to learn the ropes and see how other investors approach the process.

- Network with Other Investors: Reach out to other tax lien or tax deed investors in your area. Learn from their experience and mistakes.

- Do Your Due Diligence: I can’t stress this enough. Research the property, the title, the location, and any other liens before investing. A little research upfront can save a lot of headaches later.

- Set a Budget and Stick to It: Decide how much you’re willing to invest upfront and what kind of returns you expect. Never bid more than you can afford to lose.

Final Thoughts

Tax lien certificates and tax deeds both offer unique opportunities, and there’s no one-size-fits-all answer.

Whether you want a steady return through interest or aim to own properties at a bargain, there’s a strategy for you.

Start by understanding your state’s laws, attending auctions, and doing your due diligence.

And remember, every great investor started somewhere—your first step might be deciding if you’re a tax lien certificate kind of person or a tax deed enthusiast.

Pro Tip: You can certainly continue to research these tax liens the long way which is 100% free but very tedious and time-consuming, or you can use a high-quality research software such as Tax Sale Resources to get your time back!

Image Credit: Tax Sale Resources Homepage

They Provide:

Access To Upcoming Auctions

Access To Property Reports

Access To Over The Counter List Downloads

Access To Auction Raw List Downloads

And Much More!

Sign Up For A 7-Day Trial Today.

Finally, I believe the best way I’ve found to learn is by doing and “failing forward” as they say.

I bought my 1st investment property in 2020 during the middle of (you know what..cough..cough), and I had no clue what I was doing despite spending months researching how to invest in real estate.

But guess what? I did it.

And learned a ton of valuable lessons along the way!

So,If you’re truly interested in tax lien investing, consider subscribing to my newsletter and following along my journey from landlord to “leinlord” as a new tax lien investor.

As Leinlord grows, my goal is to provide a “behind the scenes” inside look at the tax lien auctions I participate in and thoroughly profile any properties that I win.

You’ll get to ride along with me as I walk through my risk analysis, deal structures, ROI calculations, bidding tactics, and exit strategies all documented for the world to see (even my L’s).

So please show your support and sign up for my newsletter OR if you are a Google Chrome user hit that “follow” button!

(screenshot instructions found on my about page:))

Additionally, if you’re interested in booking a consultation to talk tax lien strategy feel free to schedule a one-on-one here.

P.S. I am still fairly new to tax lien investing but willing to share what I’ve learned so far, so please keep that in mind before you book!

I’m not an expert… (yet)

Look forward to having you in the Leinlord community!

**Disclaimer

I am not a lawyer, financial advisor, or tax professional. This article is based on my research and experience as a tax lien investor. The information provided is for educational purposes only and should not be considered legal, financial, or tax advice. Always consult with qualified professionals before making any investment decisions or taking action related to tax liens. Laws and regulations vary by jurisdiction and can change over time, so verify all information independently. Investing in tax liens carries risks, and past performance does not guarantee future results.